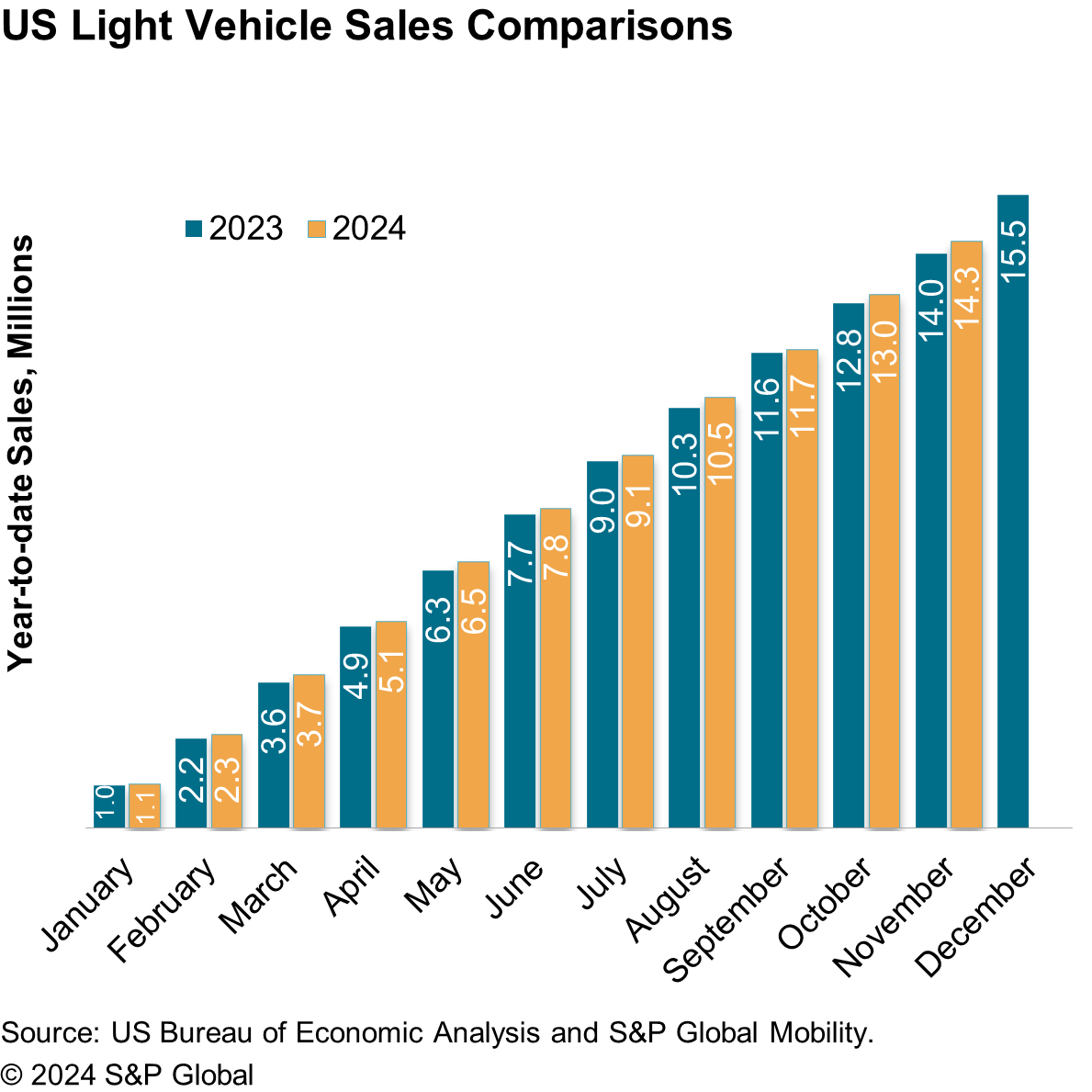

While the projected monthly volume remains familiar, retail sales levels reflect sustained advances

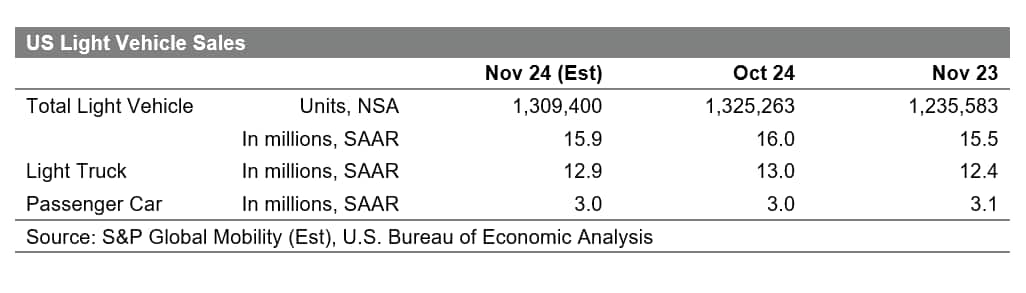

New York—On an unadjusted volume level, November US auto sales are expected to reach 1.31 million units, a growth of 6% from the year-ago level. This would translate to a seasonally adjusted rate (SAAR) of 15.9 million units, on trend with the 16.0 million unit mark realized in October.

“Retail sales are showing sustained progress in November, aided by a combination of rising inventory, the beginning of year-end clearance promotional activity, and quite possibly relief from lower interest rates,” said Chris Hopson, principal analyst at S&P Global Mobility. “The overall pace of sales would be relatively unchanged from the previous month, but advancing consumer demand could signal some easing of affordability issues.”

New inventory data also indicates that auto sales could indeed provide a happy holiday season.

According to S&P Global Mobility retail advertised inventory data, at the end of October 2024, available retail advertised inventory in the US was 3.06 million vehicles, a slight 0.2% increase over September. “This marks the second consecutive month of new vehicle inventory being over three million units, which is a high since the pandemic,” said Matt Trommer, associate director at S&P Global Mobility.

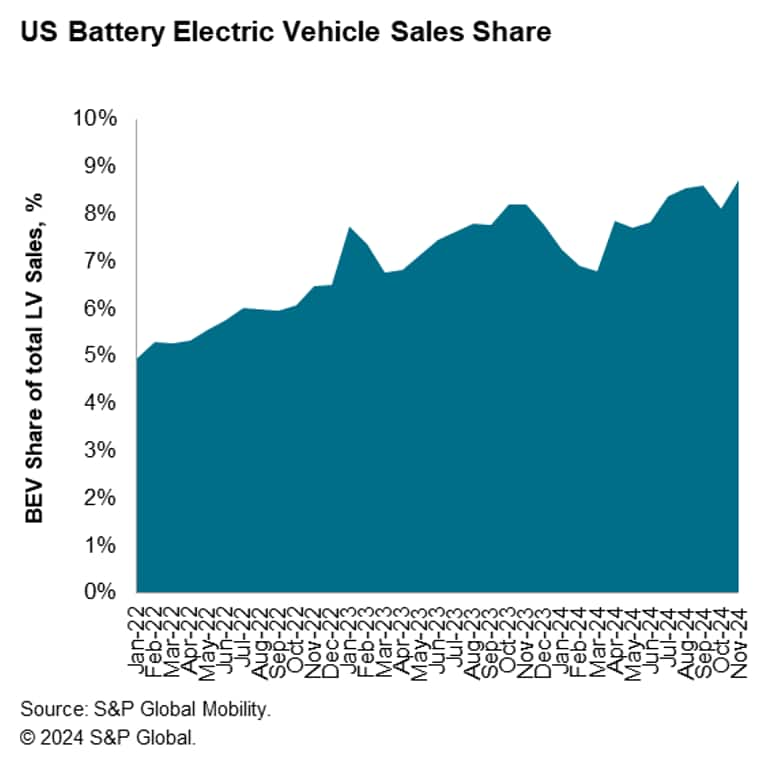

According to S&P Global Mobility new registration data, BEV share of sales has been above 8% every month since June, reflecting progress from levels earlier in the year. BEV share in September reached a level of 8.6%, with October estimated to have remained above 8% again. Despite lower inventory levels for many EVs, November and December could realize BEV share advances in anticipation of Federal EV incentives being withdrawn in 2025. S&P Global Mobility projects November BEV share to reach a level of 8.7%.

Comments are closed.