Inflation pressures and recession prospects pull sentiment lower, though focus on industry innovation remains as concerns continue over production shutdowns, weakening U.S. economy

Southfield, Mich.—According to the Q3 2022 OESA (Original Equipment Supplier Association) Automotive Supplier Barometer Index (SBI) — a gauge to measure the sentiments of North American automotive supplier executives — the outlook for the third quarter “fell deep into pessimistic territory” due to continued concerns over production shutdowns, and heightened concerns over a weakening U.S. economy.

Results reflect a highly pessimistic reading of 32 for the period, 18 points below a neutral level of 50 and a further 8 points below the already pessimistic results from Q2 2022. Sentiment deteriorated sequentially across firms of all sizes but fell drastically for mid-level suppliers. The largest, most globally exposed suppliers’ outlook remained deeply pessimistic.

The Q3 2022 OESA Supplier Barometer, sponsored by RSM US LLP, focused on Capital Markets and Innovation. The results indicate:

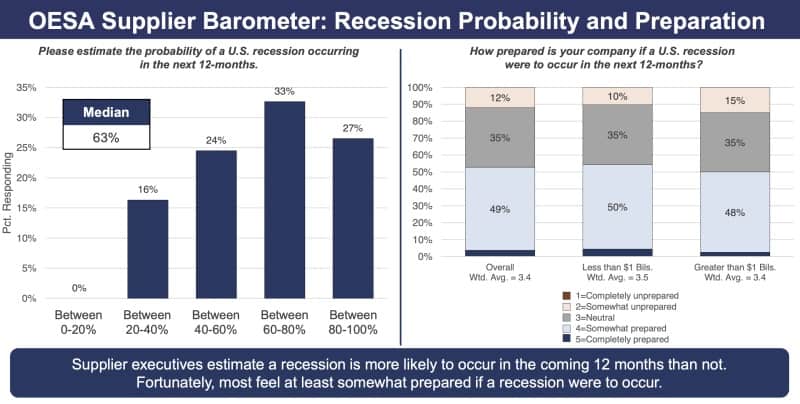

- Continued shortages of semiconductors and other components and materials continue to place immense cost pressure on the supply base. Growing concerns over the strength of the U.S. economy and continued issues with labor scarcity depressed the outlook further. Supplier executives estimate a recession is more likely to occur in the coming 12 months than not. Fortunately, most feel at least somewhat prepared if a recession were to occur.

- Capital needs are expected to broadly increase in terms of use and by company size. The industry expects the capital needed to support new program launches and production volumes will increase 4.7% and 6.2% in 2022 and 2023, respectively.

- Terms of commercial loans and credit lines are expected to continue to tighten over the coming year with the only exception being the maximum size of commercial loans. Confidence in capital acquisition remains at strong levels, and suppliers are more confident they will be able to access their needed capital in comparison to last year for all use cases.

- Forty-five percent of suppliers believe they are ahead of the industry’s pace of innovation while eighteen percent feel they are behind. Focusing on technological R&D and developing products that support the EV market are common practices by firms that consider themselves the most innovative. Firms that are catching up with the pace of the industry are investing in their engineering teams, R&D, and engaging in ongoing discussions with customers to determine their needs.

“Supplier sentiment reflects very real cost pressures due to record high inflation levels and is compounded by concerns over recessionary impacts — yet innovation strategy and sound capital expenditure planning are recognized as key drivers to mitigate such forces and bolster a stronger competitive position,” said Mike Jackson, executive director, strategy and research, OESA. “Capital needs continue to increase, fueled by higher program launch activity, product innovation, and robust R&D efforts to support advanced technologies and battery electric vehicle efforts while nearly 40% of supplier executives characterize current M&A activity as either moderate or substantial to support their innovation objectives.”

The Q3 SBI chart and a full copy of the Supplier Barometer results are available on the OESA website at: https://www.oesa.org/q3-2022-automotive-supplier-barometer.

Click here to view the RSM US LLP commentary on the Q3 2022 OESA Supplier Barometer results.

Comments are closed.