Industry reports and alternative sources paint a picture of resilient demand, tempered by policy-driven fluctuations in EVs and fleet purchases

Washington, D.C.—The U.S. government shutdown created significant hurdles for economists and analysts who depend on timely federal data. This is especially true in the automotive sector, where understanding motor vehicle demand and supply dynamics requires up-to-date statistics from agencies like the Bureau of Economic Analysis (BEA) and the U.S. Census Bureau.

As official releases were stalled, piecing together a clear picture of light vehicle sales — encompassing automobiles and light trucks — became a patchwork effort, according to a new analysis by the Plastics Industry Association.

Despite those challenges, industry reports and alternative sources paint a picture of resilient demand, tempered by policy-driven fluctuations in electric vehicles (EVs) and fleet purchases, states the report.

Official Data: Strong Signals Through August

The most recent BEA data, covering August 2025, estimates light vehicle sales at 16.4 million units on a seasonally adjusted annual rate (SAAR) — a notable increase from 15.4 million units in August 2024. This year over year growth underscores a sustained consumer appetite for light vehicles amid a stabilizing economy.

Complementing this, the U.S. Census Bureau’s Advance Retail Sales Report for August shows motor vehicle and parts dealers’ sales rising 0.5% month over month and 5.6% from the prior year. These figures align with broader economic trends, highlighting the automotive sector’s role as a key driver of retail activity.

Motor vehicles and parts manufacturing is also a vital end market for the plastics industry, with plastics comprising over one-third of the more than 30,000 parts in a typical automobile. In 2024, the value of plastics used in automobiles and light trucks reached $24.9 billion.

On the supply side, the Federal Reserve’s Industrial Production Index for motor vehicles and parts remained frozen at August levels due to the shutdown. That month, production rose 2.6% from July and 1.1% year-over-year, indicating steady output before the data blackout.

Filling the Gaps: Industry Estimates for September and October

With federal updates having been on hold, industry sources such as Automotive News, S&P Global, and Wards Intelligence had sources to bridge the gap.

September 2025

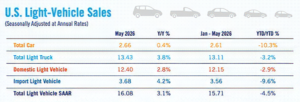

Automotive News reported light vehicle sales at 16.6 million units SAAR, a 5.0% increase from September 2024. The Automotive News Research and Data Center estimated a slightly lower 16.4 million units SAAR, still reflecting a 5.0% year-over-year gain.

This surge was largely fueled by a rush in EV purchases ahead of the $7,500 federal tax credit’s expiration under the Inflation Reduction Act on September 30, 2025. EV sales jumped 25% in September as buyers accelerated decisions.

October 2025

The momentum reversed, with Automotive News pegging sales at 15.5 million units SAAR. Early estimates vary slightly: S&P Global at 15.6 million units (down 0.6% from October 2024’s BEA-reported 15.7 million SAAR) and Wards Intelligence at 15.9 million units (up 1.3%).

The decline stemmed primarily from an 11% drop in EV sales, as consumers paused post-tax credit while awaiting potential new incentives. Fleet deliveries also fell to 22% of October sales (from 25% in September), following a third-quarter rush to preempt tariffs.

Major automakers felt the impact — GM’s fleet sales dropped 18%, and Stellantis’s fell 14% — with businesses delaying purchases amid shutdown-related uncertainties.

These shifts highlight how policy changes can create boom-and-bust cycles. The tax credit’s end without immediate replacements pulled forward September demand, only for October to see a sharp pullback in EVs and fleets.

Historical Context: Assemblies as a Recession Indicator

Supply-side resilience is further reflected in motor vehicle assemblies for automobiles and light trucks. Five of the last six U.S. recessions saw assemblies dip below 10 million units annually. Current levels, over 10.3 million units, remain well above this threshold, suggesting the industry is not yet in recessionary territory despite monthly volatility.

Reasons to Stay Optimistic

Despite data disruptions and October’s dip, several factors support a positive outlook for the U.S. automotive industry. A solid labor market, interest rate relief, and modest price increases amid tariffs will fuel strong light vehicle demand.

Job growth has cooled but remains robust, states the Plastic Industry Association’ s study. There’s a strong inverse relationship between light vehicle sales and the unemployment rate, with a -0.69 correlation on monthly data from March 1973 to August 2025. Lower unemployment typically boosts vehicle purchases as consumer confidence rises.

Recent Federal Reserve cuts have eased borrowing costs, improving affordability for automotive financing. More reductions are anticipated in 2026, further stimulating demand.

Concerns over tariff-induced price spikes have not fully materialized. The Consumer Price Index for September 2025 showed new vehicle prices up just 0.8% year-over-year. U.S. imports of motor vehicles and parts are concentrated — 93.6% from ten countries, with Mexico and Canada supplying 55.7% of parts and accessories in 2024, entering duty-free under qualifying agreements. Trade negotiations have also lowered tariffs from other key suppliers, such as Japan (8.5% of parts).

The U.S. economy, while finding its footing amid and after the shutdown, continues to provide a stable foundation for automotive demand, reports the analysis. As federal data resumes, these industry insights will likely be validated, reinforcing the sector’s underlying strength.

Comments are closed.