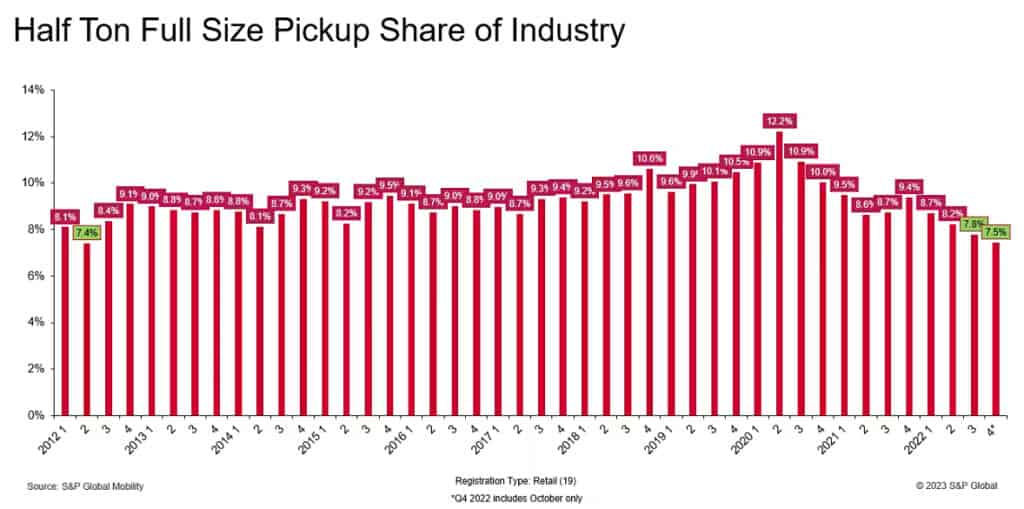

The segment’s retail shares in last two quarters of 2022 are lower than in any other quarter dating back to Q3 2012

New York—The light-duty full-size half-ton pickup segment is one of the most crucial in the US industry, for several reasons: the three segment leaders are the highest-volume models from Ford, Chevrolet, and Ram; the three pickups consistently also are the highest-volume models in the industry; there is intense sales competition among these three for bragging rights; and, it is commonly accepted that these models are highly profitable for their respective automakers.

Despite full-size pickups’ important contributions to each brand’s business case, the share of half-ton retail sales has been declining for more than two years, according to S&P Global Mobility. As shown below, the segment’s retail shares in Q3 2022 and October 2022 were 7.8% and 7.5%, respectively — lower than in any other quarter dating back to Q3 2012. It is noteworthy that the heavy-duty full-size pickup share (three-quarter/one-ton models) has been relatively steady during this time period, suggesting volume has not shifted up to this higher-profit segment.

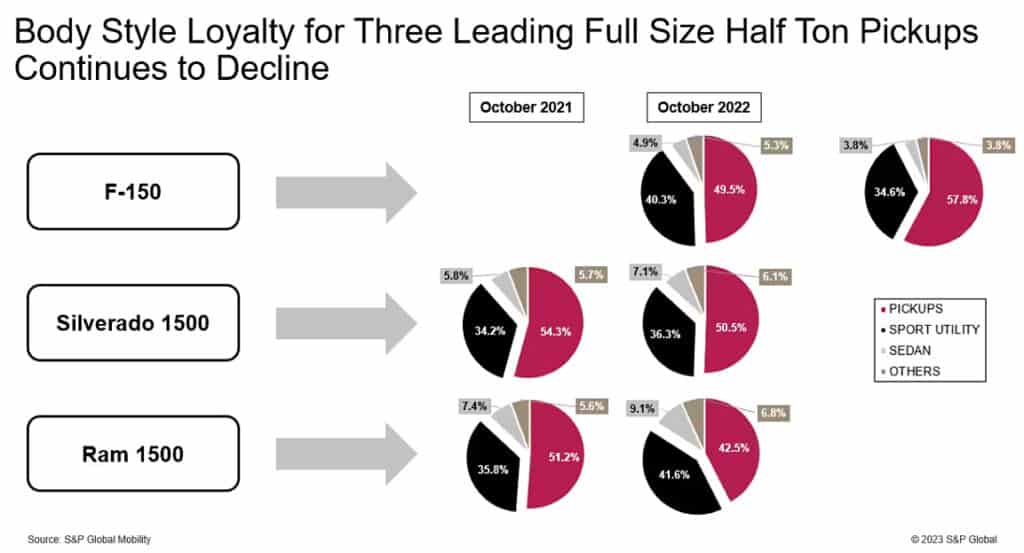

S&P Global Mobility data show these share declines can be attributed to increased migration of full-size pickup households to sport-utility vehicles. As shown below, the share of households owning each of the three leading half-ton pickups staying loyal to the pickup body style has declined in the past year, while the share moving to a utility has increased.

The change in re-purchase patterns for the Ram 1500 is the most pronounced: the percent of these owners remaining model loyal has dropped almost 9 percentage points to 42.5% in one year (Ram 1500 model loyalty peaked at 54.7% back in June 2019), while the mix migrating to a utility has climbed almost 6 points to 41.6%.

These findings align with the ongoing increased movement to SUVs from all other body styles, a predictable pattern given the plethora of utility choices available based on size, price, fuel type, sheet metal, and technologies. Through the first 10 months of 2022, utility registrations accounted for 68% of retail luxury registrations and 61% of retail registrations industry-wide.

Comments are closed.