If U.S. regulators move too fast on EV mandates over the next several years, China gains a stronger foothold in America’s EV battery supply chain — and our auto market

I’m just a car guy, but when it comes to the global auto industry, I know this: China is complicated.

First, it’s a giant auto market that’s nearly twice the size of the U.S. market. U.S. based automakers are manufacturing American-built vehicles with American labor and exporting automobiles to China. Today. That’s just the outbound.

There’s inbound too. Automotive components and finished vehicles are exported from China into the U.S., trade that supports American auto employment and customer affordability. That two-way trading relationship will grow.

It’s also true that China is both the leading electric vehicle maker and consumer in the world. Chinese automakers aren’t household names in the U.S., but BYD sold 1.9 million EVs last year and is bigger than Tesla. Great Wall Motors, SAIC and others are out there too.

Because of that sheer size (and the 15-year head start on electrification) they’ve been able to essentially corner the market on major parts of the global EV supply chain — notably the mining and processing of critical minerals (lithium, cobalt, nickel and graphite) used to produce EV batteries.

That advantage is at the heart of America’s current EV challenge:

How to accelerate the U.S. transition to automotive electrification and prevent China from locking up the global supply chains that are foundational to a successful shift?

If U.S. regulators and policymakers move too fast on EV mandates over the next several years, I predict China gains a stronger foothold in America’s EV battery supply chain and eventually our automotive market.

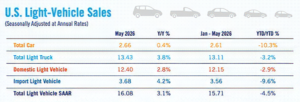

I’m talking about the Environmental Protection Agency’s proposal to require 37 percent of new light-duty cars and trucks to be battery electric vehicles by 2027, and 60-plus percent by 2030. (Last year, BEV sales were just under 6 percent).

Increased automotive electrification and carbon reduction is a mission that automakers share with EPA and the Biden administration. That should be clear enough by the EV technology we’ve championed and brought to market (97 sedans, utility vehicles, pickup trucks, vans and counting), the major battery manufacturing partnerships across the Midwest and South, and the localization of manufacturing and supply chains inside the U.S. Private sector investment of $115 billion (so far) toward electrification.

I’ve said the EPA proposal wasn’t feasible without certain public policies and in light of today’s market and supply chain conditions.

There’s not enough charging and uncertain utility and grid capacity. Here’s the big one — and where China looms largest — essentially no domestic or allied supply of battery critical minerals, processing and components until 2025 (and even then, nowhere near enough to supply what’s needed).

That’s what should be keeping policymakers up at night.

It’s hardly news that China dominates the critical mineral mining and processing universe. The U.S. imports 100 percent of its graphite. Almost one-third comes from China.

According to BMI, of the two leading components in an EV battery — the anode and cathode — China is expected to produce almost 90 percent of the anode active material and 80 percent of the cathode active material in 2030.

We just don’t mine or process these minerals in the U.S. There’s been little progress on long overdue permitting and mining reform here — and even if it magically happened overnight, it would be a decade or more before it made a material difference.

The administration still hasn’t completed a process to work with our allies and trading partners to secure those minerals either.

So, it’s a pretty grim picture on battery critical minerals despite record investments in recent years.

With that windup, what happens if EPA gets its way and requires a five-fold increase in battery electric vehicle sales in four years and a 10-fold increase in six years?

The minerals have to come from somewhere, right? Enter China and Chinese-backed mining companies in Chile, The Democratic Republic of the Congo and Indonesia.

They’ll supply the minerals and processing needed to produce the batteries — needed to build the vehicles — needed to comply with EPA’s regulation. Got that?

In other words, official U.S. policy will have thrown open the doors (and the ports, as it were) to China. Before long, Chinese automakers will accelerate their entrance into the American market with low-priced EVs that meet the aggressive (and arbitrary) EPA requirements for model years 2027-2032.

And it will be subsidized, scratch that … incentivized by American public policy. Unintended consequences … there’s no sugarcoating it.

Alarmist? I don’t think so.

Morgan Stanley recently outlined this catch-22. They described the “China case” (aka move fast like EPA proposes), the “de-risking case” (high EV adoption, with a geographically diversified supply chain), and the “slow EV case” (self-explanatory).

Here’s what they said about the China case: “The path we’re on now, despite existing legislation that attempts to incentivize onshoring, pushes rapid EV adoption which inherently increases reliance on a China-dominated battery supply chain.”

That’s my take, but it’s actually more complicated.

If the U.S. moves too slow on electrification, we’ve got a China risk, too. Failure to scale up and move with sufficient urgency gives China the running room to lock up global EV supply chains and expand into other global auto markets.

And if China moves deeper into the U.S. auto market and sells the EVs necessary to meet EPA’s mandates, it can, in turn, sell credits to American and other automakers that don’t sell as many EVs. Tesla’s been running that play for years, but this is a whole new level.

I’m talking about allowing Chinese automakers to double-dip and make (more) money precisely because EPA is requiring an electric ramp up that’s not possible — right now.

This is our Goldilocks problem. Too fast: advantage China. Too slow: advantage China.

And EPA’s proposed regulations put us in the too fast/advantage China category.

Europe offers a warning of what could happen here. The EU has prioritized the reduction of carbon emissions at the expense of almost everything else — including its industrial base. With a 2035 ban on fossil fuel vehicles looming, Chinese manufacturers gained a foothold and entered the European market at a budget price point. They achieved a 5 percent share of Europe’s EV market in the first nine months of 2022 and on a steady march to hit 20 percent by 2025.

As the New York Times recently reported: “European carmakers are frantically trying to build the supply chains they need to churn out electric vehicles.” But given generous government subsidies and other support, Chinese EV makers can’t be beat on affordability. The country’s control of battery supply chains also shields them from disruptions and price spikes.

I’m not making the case for stopping on EVs or to rely on internal combustion engines and fossil fuels in perpetuity. There’s product momentum. We can’t stop.

This is the case for getting the rules right — and balanced.

The case for weighing our climate and carbon reduction goals with national and economic security objectives. So American supply chains can catch up. So automakers can plow finite resources into the electrification future and appeal to customers on a realistic timeframe that achieves the ultimate goal: automotive electrification and carbon reduction that doesn’t set back the economy, our industrial base and consumers.

I’ll never bet against American ingenuity — especially in the auto industry, but policy and pace matter. Regulations (even imperfect ones) are designed to engineer a specific outcome.

EPA should ease up and reassess this rule before it helps cement China’s place in the U.S. auto market.

Comments are closed.