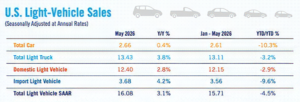

Consumers increasingly opt for non-branded parts, viewing them as of sufficient quality and better value

New York—Loyalty toward traditional OEM and supplier-branded parts continues to decline globally as consumers increasingly opt for non-branded parts (including private label store brands), viewing them as of sufficient quality and better value.

Roland Berger’s 2024 Automotive Aftermarket Pulse report shows that shops in the US and Europe in particular are installing a growing share of nonbranded parts in response to greater consumer price sensitivity. This contrasts with China, however, where consumers lack confidence in non-branded parts.

The report, which surveyed 600 repair shop owners and managers and 6,000 private car owners in 13 global markets, including the US, China, Germany, UK and France, assesses how evolving preferences will impact choices for vehicle repair and maintenance in the year ahead. This year, the study covers all major American markets: US, Canada, Mexico and Brazil.

Car owners worldwide reported spending more in 2024 on the upkeep of their cars, with U.S. and European consumers in particular increasing repair and service spending at a rate that outpaced inflation. Forty-eight percent of US consumers reported spending between $330 to $700 during the year on service, maintenance or repair during the year, with 25% saying they spent more than $700.

“The report highlights that global suppliers can unlock a competitive edge by tailoring regional strategies to local preferences for branded vs. non-branded parts,” says Elena Yakushkina, Principal, Roland Berger.

Neury Freitas, Partner, Roland Berger, adds, “For instance, in markets where brand loyalty of consumers is high, suppliers can focus on premium branded offerings, strong warranty packages, and brand-specific marketing. In regions favoring cost effective options, they could emphasize reliable non-branded parts with a streamlined distribution network to enhance affordability.”

Additional findings from the report include:

• While EV penetration has been seen as a tailwind for the OEM service channel, an overwhelming majority of EV owners globally (76 %) say they would take their vehicle to an independent shop for simple maintenance or repairs. Nearly 50% would take their vehicle to an independent shop for powertrain or battery related issues.

• More consumers than ever (51%) are buying parts online, but they continue to express frustration with the user experience of the channel. Forty-eight percent of US consumers reported that they bought parts online in the past year and would do so again. In Europe, a growing number of online parts buyers are opting for the online-to-offline (O2O) model where the parts are installed professionally.

• U.S. consumer preference for IAM repair shops over OEMs continued to grow in 2024, with 56% of respondents choosing independent workshops, compared to 50% in 2023, due to lower prices and shorter wait times offered. This contrasts with China, where the popularity of OEM repair shops is growing driven by EV owners and the efforts of Chinese EV OEMs to optimize customer experience and convenience at their workshops.

• Vehicle owners around the globe are showing more interest in sustainable parts, for example 77% in 2024 vs. 64% in 2023 in the US. However, relatively few are willing to pay a premium for a green part, which opens an opportunity for the remanufacturing business.

To download the Roland Berger 2024 Automotive Aftermarket Pulse Report, please visit: B2B and B2C trends in the automotive aftermarket | Roland Berger

Comments are closed.